What companies should now consider when providing cross-border services

Many internationally active companies assume that a German branch automatically triggers German VAT. However, it was precisely this view that the Federal Fiscal Court significantly restricted in its ruling from December 4, 2025 (V R 37/23).

At the heart of the matter is a question that regularly leads to uncertainty in practice: When is Germany actually the place of performance for cross-border services and when is it not?

This distinction can have considerable tax implications, particularly for international corporate structures, sales offices, holding companies or cross-border services. The ruling brings more clarity here and should be particularly relevant for companies with international service relationships.

What was the case about?

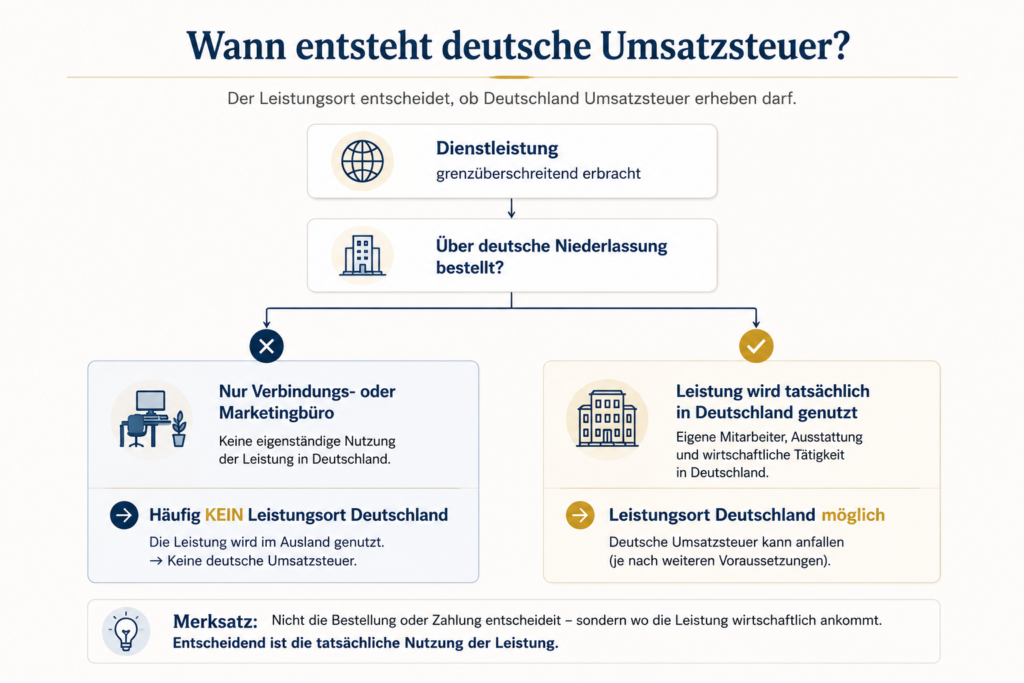

In the case in question, a company was based outside the European Union but had a liaison or marketing office in Germany. Advertising services were ordered via this German branch. However, the services were used exclusively for the company’s foreign business.

The tax authorities initially took the view that Germany was the place of performance, as the services were obtained via the German branch. The Federal Fiscal Court took a different view.

According to the BFH, it is not only the branch office through which services are ordered or invoiced that is important. Rather, the decisive factor is where the services are actually used commercially.

The BFH is thus once again strengthening the economic approach in VAT law.

When does a permanent establishment really count?

The ruling makes it clear that a German permanent establishment does not automatically “move” the place of performance to Germany. Rather, the decisive factor is whether the branch in question actually uses the service for its own economic activity.

The BFH closely follows the previous case law of the European Court of Justice. In particular, the decisive factor is whether the branch is in a position in terms of personnel and organization to use the respective service independently.

A mere representative office, a marketing office or an administrative unit is often not enough.

This point is particularly important in practice because many companies procure international services centrally via certain companies or branches, but the actual use takes place elsewhere.

BFH and tax authorities assess the practice differently

The ruling is particularly interesting because it differs in part from the previous administrative opinion.

In practice, formal criteria have often been the main focus to date. In particular, the VAT identification number used often played a central role. If a service was procured using a German VAT ID number, there was much to suggest from the perspective of the tax authorities that Germany was also the place of performance.

The BFH takes a much more differentiated view of this. Although the VAT ID number used can be an important indicator, it does not replace an actual examination of economic use.

The ruling thus creates more leeway for companies that can properly document international performance structures.

Why the ruling is relevant for companies

The ruling affects significantly more companies than one would initially expect. International corporate groups, SaaS companies, agencies, consulting firms or holding structures in particular often work with cross-border services and multiple branches.

In tax audits, disputes regularly arise as to which country services are actually attributable to and whether German VAT is due.

It often becomes particularly problematic when services are formally provided via Germany but are used economically for foreign business areas.

In the absence of proper documentation, considerable tax risks quickly arise.

What companies should consider now

In future, it will be even more important for companies to be able to document the actual use of services in a comprehensible manner. This is less about formal organizational charts and more about the practical question of which company or branch actually uses the respective service.

Service providers should also not allocate cross-border services solely on the basis of the VAT ID number used. A closer look is often worthwhile, especially in the case of more complex international structures.

The ruling does not mean that previous practice will change completely. However, it strengthens companies that structure and document international service relationships in an economically sound manner.

Conclusion

In its ruling, the Federal Fiscal Court clarifies that formal criteria alone are not decisive for the place of performance. Neither the VAT ID number used nor the mere fact that the order was placed via a German branch automatically means that Germany is the place of performance.

In the end, it depends on where the power is actually used economically.

Particularly in the case of international services and complex corporate structures, this delimitation can have a considerable impact on VAT. This makes it all the more important to analyze service relationships properly and document them in a comprehensible manner. This makes it all the more important to analyze service relationships properly and document them in a comprehensible manner.

At Taxboutique by Julia David & Edda Vocke, we support companies in the tax classification of cross-border services and in preparing for VAT audits.

1

Inquiry & initial consultation

You fill out our short questionnaire – 3 minutes. We will get back to you within 48 hours with an appointment proposal for a free initial consultation.

Free of charge & without obligation

2

Analysis of your situation

We analyze your initial tax situation, identify potential and show you specifically what we can do for you – with clear figures.

Usually 3-5 working days

3

Strategy & Structure

Together, we develop your personal tax strategy – whether it’s the choice of legal form, holding structure or structuring optimization. Everything is documented and traceable.

Personally at partner level

4

Implementation & ongoing support

We take care of all tax matters – digitally, structured and proactively. You will receive regular updates, deadline reminders and direct access to your advisor.

Fully digital